Financial Reports: Home Depot, CNH, Kubota

Home Depot up 6%

On Nov. 12, The Home Depot reported sales of $40.2 billion for the third quarter of fiscal 2024, an increase of 6.6% from the third quarter of fiscal 2023. Year to date, Home Depot reports sales $119.8 billion, a 1.6% gain over the $117.8 billion YTD 2023. Comparable sales for the third quarter of fiscal 2024 decreased 1.3%, and comparable sales in the U.S. decreased 1.2%.

Sales details

- Q3 2024 Average ticket, $88.65, off less than 1% compared to Q3 2023 ($89.36)

- Q3 2024 Sales per retail square foot, $582.97, off 2% compared to Q3 2023 ($595.71)

The company’s Q3 sales gains are due in part to its acquisition of SRS Distribution, and to consumer need to protect and repair in hurricane-damaged areas. The gain beats the company’s previous outlook estimate of growth between 2.5 and 3.5%. The company said that sales related to hurricanes Helene and Milton contributed about one half a percentage point of sales growth to the quarter.

“While macroeconomic uncertainty remains, our third quarter performance exceeded our expectations,” said Ted Decker, chair, president and CEO. “As weather normalized, we saw better engagement across seasonal goods and certain outdoor projects as well as incremental sales related to hurricane demand. I would like to thank all of our associates for their dedication in serving our customers and communities.”

Outlook

- Total sales to increase approximately 4% including SRS and the 53rd week

- 53rd week projected to add approximately $2.3 billion to total sales

- SRS expected to contribute approximately $6.4 billion in incremental sales

- Comparable sales to decline approximately 2.5% for the 52-week period compared to fiscal 2023

- Approximately 12 new stores

- Gross margin of approximately 33.5%

- Operating margin of approximately 13.5%

CNH drops 22%

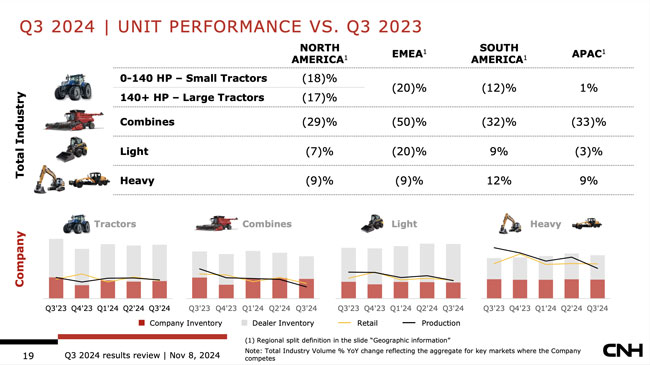

CNH Industrial reported results for the three months ended September 30, 2024. Its consolidated revenues were $4.65 billion (down 22% compared to Q3 2023) and Net sales of Industrial Activities were $4.00 billion (down 25% compared to Q3 2023). The manufacturer also lowered its full year 2024 guidance to reflect continued weak end markets and elevated channel inventory levels.

“With the current challenging market conditions facing farmers across the globe, CNH is implementing decisions to advance our transformation journey. We have focused on making the Company’s operations more efficient and on being more responsive to our customers’ needs. But dealer inventories remain elevated and will require additional efforts to align with retail demand. As we further adjust production levels while making investments in technology and quality-improving processes, we are positioning ourselves for the long term and cementing our leading position in the industry. We look forward to sharing more details of our strategy at our investor day on May 8, 2025,” wrote CEO Gerrit Marx, in a statement.

The decline in Net sales of Industrial Activities is mainly due to lower shipments on decreased industry demand and reduced dealer inventory requirements. In North America, industry volume was down 18% year-over-year in the third quarter for tractors under 140 HP and was down 17% for tractors over 140 HP; combines were down 29%. The company reported that sales were down worldwide, except for the Asia Pacific region, where it said tractor demand was up 1%.

Global industry volume for construction equipment increased 1% year-over-year in the third quarter for Heavy construction equipment; Light construction equipment was down 9%. Aggregated demand decreased 16% in EMEA and 7% in North America but increased 11% in South America and 3% in Asia Pacific.

Construction net sales decreased for the quarter by 28% to $687 million, due to lower volumes driven mainly by a decrease in market demand across all regions.

2024 Outlook

The company said it will reduce production levels after forecasting continued weak industry retail demand in both the agriculture and construction equipment markets, coupled with elevated dealer inventories. Due to the lower productions levels, CNH is revising its segment net sales and margins and its EPS results.

- Agriculture segment net sales down between 22% and 23% year-over-year including currency translation effects (from down 15% to 20% previously)

- Construction segment net sales down between 21% and 22% year-over-year including currency translation effects (from down 15% to 20% previously)

Kubota Global reports slight gain

For the North American market, Kubota reports steady demand of infrastructure development in the CE market. The demand of housing market is calm although it is soft. In the tractor business, the residential market has been slow due to slowdown in business sentiment. The agricultural market also slowed down due to crop prices decline.

For the nine months ended September 30, 2024

Revenue (in billions of yen)

- Q3 2024, 2,277.9

- Q3 2023, 2,258.2

- Difference +19.7

- Percentage +0.9

That is for all of Kubota Global, of which Machinery comprises 2,017.1 billion yen. In other parts of the world, Kubota reported its sales were off YOY in both Japan and in Europe. The company reported strong YOY revenue gains in Asian nations other than Japan.

In a separate monthly sales report for the U.S. market in October 2024, Kubota reported:

- Tractor sales were down double digits YOY

- Mower & RTV sales were up by double digits

- CE sales were +2~10%