Q4 OPEB 2021 Industry Pulse

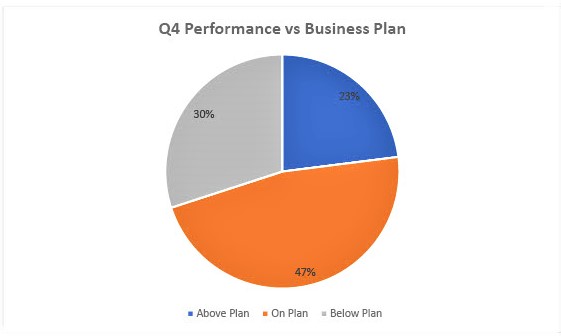

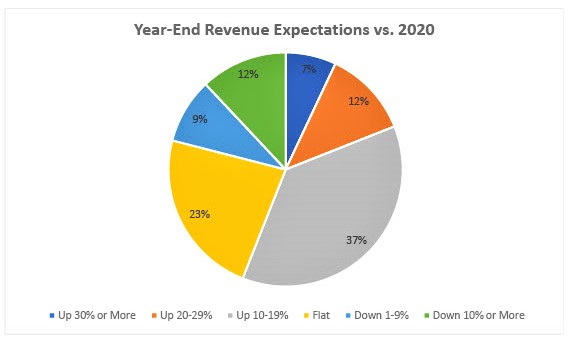

Despite a stalled supply chain and the resulting inventory issues in 2021, nearly 60 percent of dealers say they expect their year-end revenues to exceed 2020’s numbers, according to our OPEB Q4 dealership survey. In addition, 70 percent of surveyed dealers indicate their Q4 performance was at or above plan.

Beyond supply-chain challenges, dealerships cited various other risk factors going forward, including: the U.S. political environment; high/rising gasoline prices; the employment outlook; economic/political issues outside the U.S.; Covid; consumer financing costs/availability; tariffs/trade wars; and the housing market.

We surveyed more than 100 outdoor power equipment dealers in 37 states to get their insight on their business and the current state of the OPE industry. Ninety percent or more of respondents were independent, single-location dealerships.

What follows are the latest results from the OPE Business Q4 dealership survey for 2021. You can view our Q3 OPEB Industry Pulse results in our November/December issue (page 34).

(Editor’s note: Note that in the bar charts, the keys below the bars always read left to right.)

Annual Dealership Revenue

Our surveyed dealers represented a mix of all revenues.

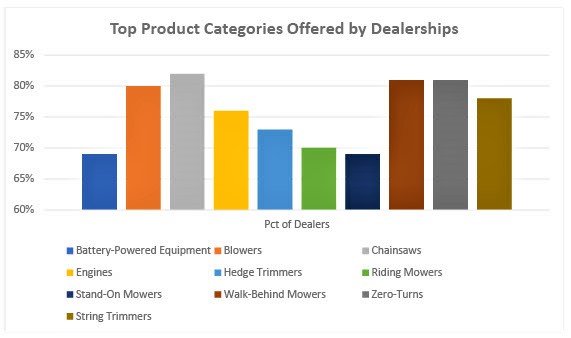

Top Product Categories

80% or more of dealerships indicated they offered chainsaws, zero-turn mowers, walk-behind mowers and blowers.

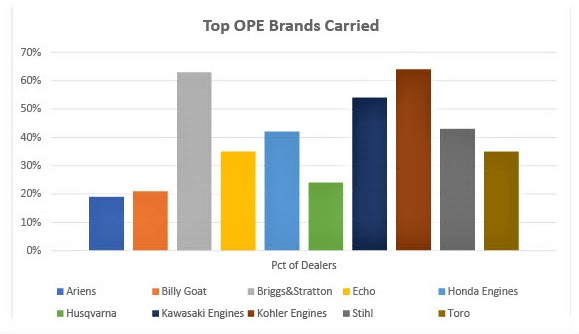

Top Brands Carried by Dealerships

We asked dealers which OPE brands they carried — these are the top 10 brands reported by responding dealerships.

Other brands noted by at least 10% of responding dealers included: Cub Cadet (11%), Exmark (18%), Generac (11%), Gravely (18%), Honda Power Equipment (16%), Hustler (12%), Mantis (16%), MTD (14%), Red Max (17%), Scag (11%), Shindaiwa (11%), Simplicity (12%) and Snapper (15%).

Q4 Performance vs Plan

70% of dealerships indicated their Q4 performance in 2021 was on or above plan.

Year-End Revenue Expectations

A majority of dealers (56%) indicated they expect year-end revenue expectations to exceed revenues in 2020.

Profit Margins in 2021

Nearly half of all surveyed dealerships (49%) said their profit margins in 2021 were somewhat better or significantly better than 2020.

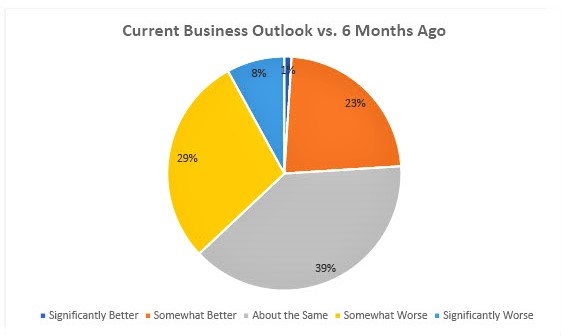

Dealership Business Outlook

We asked dealerships, “In general, to what extent has your business outlook changed compared to 6 months ago?”

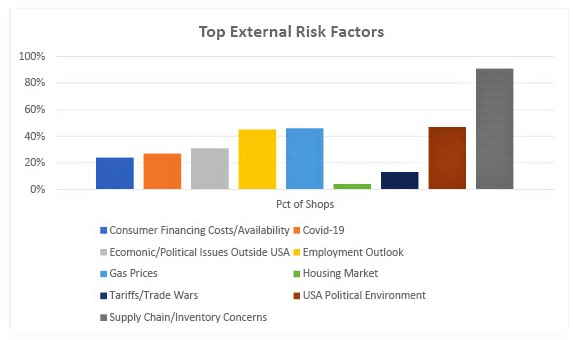

External Risk Factors

The top dealership concerns for the future when it comes to external risk factors? No surprise here: the supply chain and inventory concerns lead the way by a wide margin.

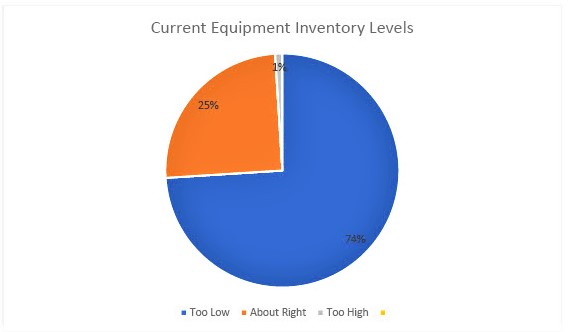

Inventory Levels

In characterizing their dealership’s current inventory levels, nearly three-quarters of all dealers (74%) noted it was too low.

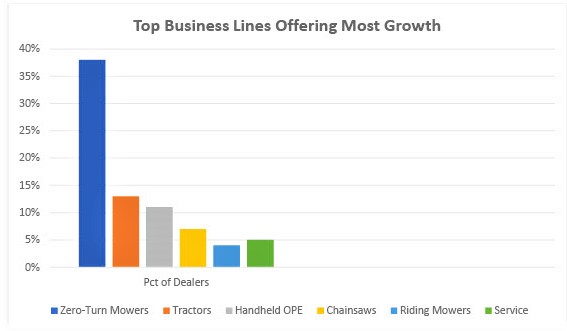

Top Business Lines for Growth

What lines of business provided dealerships with the most growth in the past quarter? Zero-turn mowers, by a large margin (38%).

Dealer Comments

Finally, we’ll share just a few of the dealer comments from our Q4 survey (we are honoring our pledge of anonymity here):

- “Very frustrating year with big time supply issues! Could have done another million in sales if we could have gotten equipment.”

- We have seen some serious supply-chain problems mainly in new equipment. Never received most of our spring booking from all manufacturers. If we have the inventory, we are able to sell it.”

- The new mowers that I ordered in March are just now beginning to trickle in. I got two last week and will get two next week. I have lost a lot of sales because I couldn’t get anything to sell. The salesmen have been telling me it will not be any better in 2022.”

- “Distributors are cutting SKUs and profit margins while increasing demands such as marketing percentages, and not guaranteeing product to sell.”

- “The box stores need to be required to follow the same rules as the independent dealers with the manufacturer.”

- “Very concerned with manufacturer loyalty to the dealer channel. Supply-chain issues are still hurting our business.”

- “Not enough products to sell. People do their research and want something specific, but it is not available to order and other dealers will not transfer because they know they’ll not be able to get a replacement.”

- “Spring is going to be very busy with service work, but new sales will remain poor [due to] availability of product.”

- “Dealers need to focus on profit as margin, not dollars. Too many dealers [are] low-ball pricing, leaving a lot of money on the table just to get the sale! seems to be a race to the bottom.”

- “Profits are up on new equipment. This is a trend that needs to continue after the supply-chain issues. I feel like this is a major bright light in the supply-chain uncertainty we’re all dealing with.”

- “Although the numbers are up, the profits are down. I believe it’s a combination of rising supply costs, rising wages and the inability to maintain a substantial staff to handle the workload. I have noticed a recent lack of high-dollar new equipment sales but an increase of older equipment refurbishing.”

- “We’re seeing fast-rising costs but profit levels remaining the same or falling. The biggest concern is the retail finance cost we’re having to pay. Interest rates continue to be historically low but we’re seeing the highest finance costs we have ever seen. Freight costs (wholegoods and parts) are continuing to rise.”

- “The future of outdoor power equipment looks troubled, as margins continue to decrease and retail pricing increases, along with the supply issues we face – not to mention freight costs and the increased minimums imposed from our distributors and manufacturers. I think it will be a challenge to remain profitable moving forward. Manufacturers need to realize there simply isn’t enough margin in this industry to support qualified employees to help run these small businesses. This is why we see an increase in the diversification of the hardware retailer and the outdoor power equipment industry, along with the decrease of outdoor power equipment dealerships. I think dealers will need to be cautious as to who they partner with moving forward as there seems to be very few, if any profitable solutions.”

- “Our younger employees are being tempted by the fact that the minimum-wage debate has caused fast food places to offer more per hour to start than our normal starting wage for an entry-level job.”

- “Plenty of business, but not enough employees to handle the workload. I have to put in 12-hour days, 7 days a week.”

- “Has been very challenging the past 2 years. Enormous growth, but not able to handle [it] due to low employment numbers – it’s almost impossible to get good, qualified help.”

- “Product availability and finding qualified employees are the two biggest problems.”